Global IMS Market 2010

Release Date:2011-01-17

October 2010, selected from market research firm iLocus

An Overview of IMS Deployment Scenario

There are three types of operators that have steadily been deploying IMS technology over the last few years. The first category of operators is those that have IP to the edge. These include wireline operators, cable operators, certain commercial LTE network operators, and WiMAX operators. These service providers have been able to use IMS core to offer telephony services. The second type includes mobile operators that do not have IP to the edge yet and are therefore not able to use IMS core for telephony services. The third category includes service providers who have both wireline and wireless networks. This category of service providers are driven by FMC for lower TCO, and are focusing mainly on their enterprise customers, offering services such as convergent centrex that often uses a common IMS core.

Obviously most of the IMS action surrounds the wireline market where the packetization has been pushed to the edge through broadband deployment. For convergent operators, IMS solves time to market issue. For mobile operators, the short term driver is to launch the enhanced communications services like RCS. But that is a major market driver. It is not a sufficiently large enough motivation to go for IMS deployment. But since the industry chose IMS to carry VoIP within mobile networks the mid term driver for IMS is VoLTE.

IMS Deployments in Wireline

In the Class 5 space what we saw was hybrid TDM switches being built so that operators could begin to put IP in the middle to do VoIP. Operators did not necessarily do direct IP termination but they put IP in the middle. Some vendors had architectures that allowed them to do that easily. And that is what drove a lot of consumer VoIP or VoIP termination in the network. That was early on. Now if we move to today’s network we see the urge to utilize the broadband infrastructure and that mandates IMS type deployments. Most markets have alternative broadband service providers either wholesale or ULL. So broadband is taking off.

There is a shift from softswitch/NGN implementations to all-IP IMS implementations. However in numerous cases operators are bypassing the softswitch implementations moving straight from PSTN to IMS. These include carriers like Turk Telekom, Telkom Malaysia and many others. Move to softswitch was not really a move to IP. A softswitch network is still TDM oriented using IP mainly as transport medium. IMS is pure IP. That seems to be the top most trend in the market these days.

On a cumulative basis (as of end 1H10), a total of 207.9 million IMS subscriber lines have been shipped for deployments across both wireline and wireless networks. Of these an estimated 134.8 million lines have been deployed in wireline networks. Estimated 30.9 million lines have been installed in wireless networks and around 42.2 million deployed in convergent IMS deployments.

An estimated 25% of the total subscriber capacity in wireline networks has migrated to VoIP. Of the 25%, around 14% is comprised of softswitch based subscriber lines and remaining 11% is comprised of IMS based subscriber lines.

Majority of the 75% of the subscriber lines in wireline segment that remain TDM based are likely to be migrated direct to IMS. By the year 2014, the ratio of IMS-to-softswitch based subscriber lines deployed in the wireline networks is forecast to be around 2:1.

During 1H10, estimated 18.8 million IMS subscriber lines were shipped for deployment in wireline networks worldwide. Out of the 18.8 million IMS subscriber lines shipped in 1H10, an estimated 1.3 million were for IP centrex lines. The remaining 17.5 million were residential lines. Figure 1 gives vendor market share in residential IMS subscriber lines for the year 1H10. Ericsson leads the market with 24% share worldwide followed by ZTE with 22.3% and NSN with 18.9%.

IMS Deployments in Wireless

The main driver that will bring IMS to wireless market is LTE when users have IP to the edge. There is not much opposition to the premise that doing voice over LTE is by using IMS. So just like on wireline side you had to wait till broadband kicked in, on wireless side you have to wait till IP hits the edge. Mobile broadband has seen a sharp increase over the years. However we still do not have IP to the edge. The shift to LTE will in most cases be associated with IMS deployments to support voice. In the remaining cases that use some interim option, they will over time also move towards IMS. So it is a matter of when an operator starts LTE deployment.

With the use of Mobile Access Gateway Control Function (MAGCF), however, the operator does not need to have LTE in place in order to utilize an IMS core. Broadly speaking there are two scenarios: (1) where operator has deployed LTE but voice still traverses its softswitch network. In this scenario, operators evolve the present softswitch in order to handle VoIP. Classic method includes that of NSN’s MSC VoIP server solution whereby the VoIP application server APIs are opened up to hook with the MSC. The other major solution in this scenario is CS fallback in which case you need two radios in the handset. (2) In the second scenario where an operator does not have LTE in place but is looking to use IMS core, there are MAGCF solutions being developed by vendors. ZTE has a commercial version available in the market. This solution is important from operator perspective because a lot of investment has gone into softswitch in mobile space.

In MAGCF deployments, mobile softswitch acts as softswitch and MAGCF at the same time. Softswitch handles all users except those users who want IMS services which are handled by MAGCF part which will send all call control to IMS core.

MAGCF is the mobile version of fixed AGCF which has been around for a while now. It is about providing access gateway function for narrowband users to IMS core. Fixed AGCF is mature now. Mobile AGCF is not mature yet. Only ZTE has released a commercial product. Most other vendors will release MAGCF product towards the end of this year. It is a software upgrade to mobile softswitch to convert part of the softswitch module into MAGCF component.

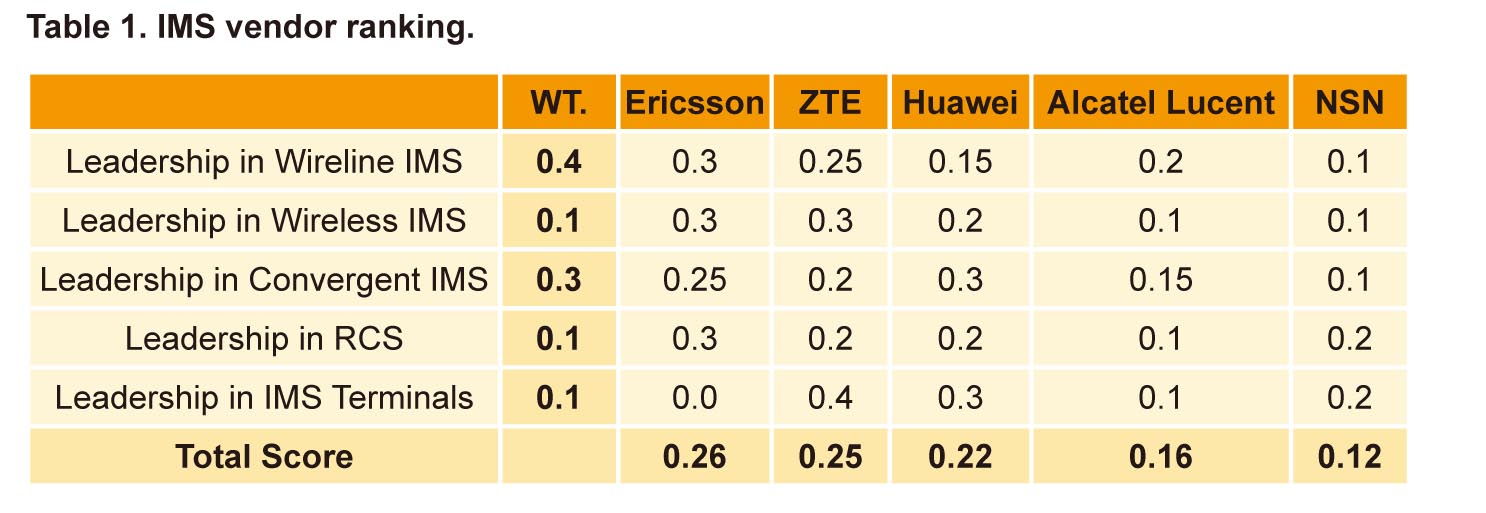

A Ranking of IMS Vendors

All large vendors are thinking only in one direction and that is IMS, even though these vendors still generate more revenues in softswitch deployments than in IMS. There are only a handful of vendors out there who are up to the IMS challenge, however. It is the same large vendors. This is not a market that mid tier vendors can effectively address. The players that will dominate the scene will be the usual suspects: Ericsson, ZTE, Alcatel-Lucent, NSN and Huawei.

Between the five of them, some have excelled in wireline IMS deployments while the others have excelled in convergent IMS deployments. We have identified the following factors as the main criteria for ranking the five vendors:

■ Leadership in Wireline IMS

■ Leadership in Wireless IMS

■ Leadership in Convergent IMS

■ Leadership in RCS

■ Leadership in IMS Terminals

We think these are the most important and most relevant indicators given the way IMS market has matured so far. The most active area of IMS is undoubtedly the wireline segment. As such, in terms of relative weightage of these five factors, we have to assign the wireline deployments a higher weightage. After wireline, the most active deployment area in IMS is the FMC type convergent deployments such as convergent centrex. There is not much IMS deployment in wireless-only networks. We have given this area the same relative weightage as RCS and terminals. So our relative weightages are proportional to the extent of related deployments.

Ericsson emerges with the top rank followed by ZTE at number two. Ericsson is strong in all three important areas of IMS right now: wireline, wireless, convergent scenarios. ZTE has leadership in wireless and terminals side, with a strong performance in wireline IMS during 2009 and 1H10. ZTE is the only vendor there with a commercial MAGCF product in the market.