Market Share Alert: 3Q11 Global ON

Release Date:2012-03-28

By Dana Cooperson, OVUM

Annualized spending grew, but 4Q11 outlook appears less rosy

Summary

In a nutshell

With most of the top-line vendor revenue data confirmed, preliminary results indicate that despite a sequential dip in quarterly spending in 3Q11, annualized global optical networking (ON) spending rose to $15.5bn. Although a sequential decline is seasonally consistent with most third calendar quarters and, therefore, ordinarily no cause for alarm, our quarterly vendor calls and recent market reporting, including many earnings announcements up and down the food chain, point to a deteriorated outlook for 4Q11. Spending in all regions was down sequentially, but only in North America was it down year over year. Vendor results were mixed: Alcatel-Lucent, Tellabs, Ciena, Ericsson, and Nokia Siemens Networks (in descending order) each lost rolling 4Q share; Huawei and NEC were flat; and ZTE, Cisco, and Fujitsu (in descending order) all gained. We are running ahead of our $14.9bn forecast for the year and are unlikely to miss the forecast. The main cause for alarm beyond 4Q11 is that the anticipation of worse times ahead could create them, as market players act more conservatively than is warranted by underlying market conditions.

Ovum view

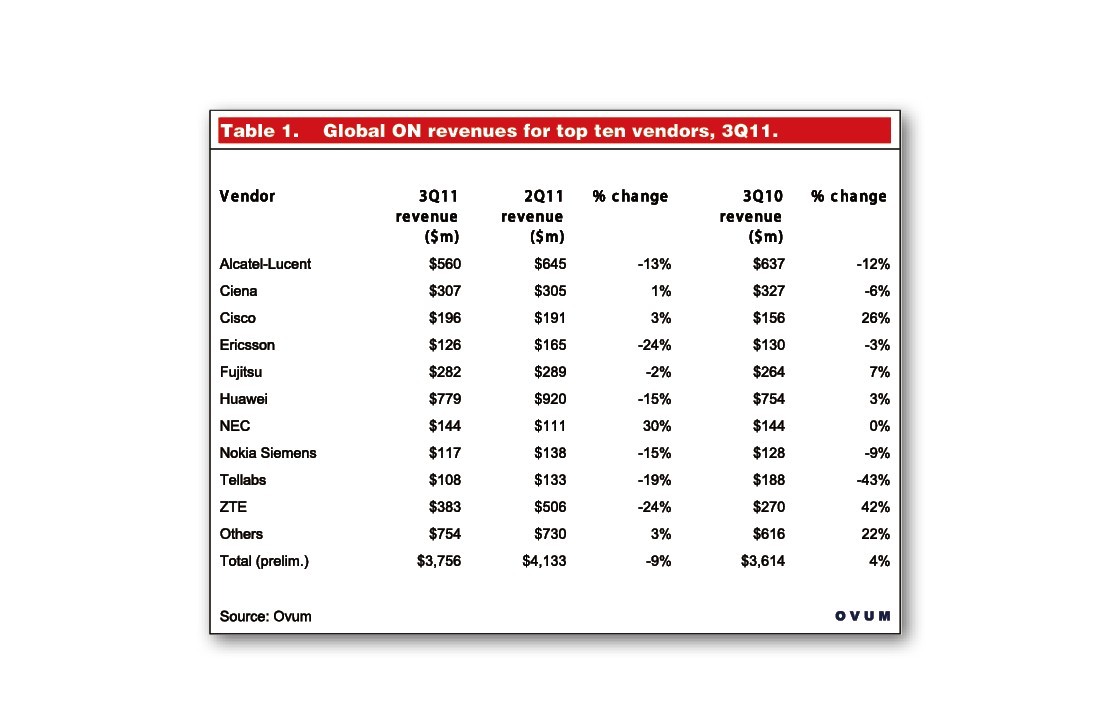

Preliminary results indicate that the climb up from the 2Q10 market trough continued in 3Q11. Revenues rose to $3.8bn, down 9% compared with 2Q11 but still up 4% compared with 3Q10. Of most comfort to market watchers and players, annualized spending was up 9% compared with 3Q10 to $15.5bn. This marks the third and best sequential quarter of annualized spending gains versus the year-ago period and puts the market more than halfway back to its pre-recession peak of $16.6bn, posted in 3Q08. Spending continued to shift away from legacy bandwidth management and aggregation to DWDM and converged packet optical (CPO) products, with ROADM and 40G/100G being growth hotspots. Revenues for new products with OTN switch capabilities inched up, but many of these products remain in customer lab and field trials.

As 3Q11 unfolded then progressed to 4Q11, general market sentiment turned more cautious and negative than we’ve registered in over a year. For example, Infinera proactively warned about the likely 5−15% negative impact on its revenues in 4Q11 due to flooding at its Thai contract manufacturer. But due to second-sourcing and inventory on hand, other vendors reported very little expected impact. We did, however, hear material reports of the big North American service providers, most notably AT&T and Verizon, pushing deliveries into 2012. Spending was off sequentially the most in percentage terms in North America and EMEA. Consequently, results tended to be the most negative for the top ten vendors with more than 50% of their revenues coming from those two regions; only Cisco and Fujitsu bucked this trend.

Key messages

● ZTE gained the most share for the second 4Q rolling period in a row: ZTE gained 0.6 share points in the 4Q10−3Q11 period, matching its performance last quarter. Cisco followed with a 0.2 point gain and Fujitsu with 0.1 points.

● Number one Huawei increased its share lead over number two Alcatel-Lucent: Huawei had no loss or gain in annualized share, but since Alcatel-Lucent topped the list of vendors with a 0.7-point share decline, Huawei increased its lead. NEC also registered neither a gain nor a loss, while Tellabs, Ciena, Ericsson, and NSN joined Alcatel-Lucent in the loss column.

● Performance to forecast: Ovum published an updated forecast in June (see ON Forecast Report: 2011−16). Annualized market spending increased to $15.5bn, which is 4% over our 2011 most likely forecast of $14.9bn. Of the product categories we track, through 3Q11 bandwidth management and SLTE are underrunning our forecast while all other categories are overrunning. Fear of worsening economic instability in Europe and the US is leading to caution up and down the food chain and appears likely to have a negative impact on ON spending in 4Q11 in those markets. However, it remains unlikely that performance in 4Q11 will be so bad that spending for the year will dip below $14.9bn. China is likely to play a big part in the final global spending tally.

● DWDM and packet continue to drive market growth: Spending for DWDM passed 50% of market spending for the first time in 3Q11 (both for the quarter and the rolling 4Q period), even as annualized aggregation spending was the strongest we’ve seen in over a year. SLTE spending remained disappointing despite lots of activity. Bandwidth management continued to sink, dropping below $1bn annualized for the first time and highlighting Tellabs’ troubles.

Key market trends

● OTN switch sales are being driven by 40G/100G terrestrial and subsea network upgrades, along with international and high-capacity leased lines. While Huawei, Infinera, and ZTE have been shipping OTN switch fabrics for revenue for years, Ciena and Tellabs shipped for revenues starting in 2Q11, and Alcatel-Lucent and Ericsson did so in 3Q11. NSN is shipping for trials, but not yet for revenues. ECI announced a new OTN-capable series, the Apollo OMLT family, just after the end of the quarter (see ECI’ s Apollo OMLT: a new kind of god (box)?). We expect at least one more vendor to announce OTN switch capability by the end of the year or early in 2012.

● 40G/100G growth continues; more vendors ship product: Growth in 40G and 100G shipments continued in the quarter. The need for better reach and better performance on high-PMD fiber pushed 40G coherent sales, while Fujitsu joined the list of vendors offering 40G coherent during the quarter. Among the top ten, Alcatel- Lucent and Ciena still have the coherent 100G market mostly to themselves. Huawei says it has shipped both coherent and non-coherent 100G; ZTE notes non-coherent shipments, with coherent being available for field trial in 2H11; Ericsson and NSN expect to ship 100G coherent for revenue in 4Q11, with Cisco, Fujitsu, NEC, and Tellabs following suit in 2012. 40GE and 100GE remain very rare to date, although we expect this to change in 2012. A more complete update on 40G/100G will be available in our full share report.

● MPLS-TP still largely a future need; enterprise services and backhaul are pushing Ethernet-based transport. Vendors routinely report that only about 25−30% of aggregation product client interfaces are Ethernet, with some vendors citing mobile backhaul and others enterprise services as the leading growth driver. Most vendors are implementing both an MPLS-TP and IP/MPLS control plane in their edge products, as there is no clear consensus from customers which way they will want to go for what applications.

● The cloud’s impact on ON is…loud: For the most part, where carrier infrastructure is concerned, the impact of the cloud remains hazy. In preparation for our upcoming cloud report, we asked vendors for any special requirements they are seeing from customers and if there were any leading service providers and we came up almost empty. Encryption/security, low latency, self-service portals for end users looking to commandeer bandwidth on demand, and “extreme reliability” were some likely requirements that vendors did suggest.

3Q11 Results

Global revenues up 4% compared with 3Q10, but down 9% sequentially; half of the top ten vendors’ revenues declined year over year

Year-over-year global spending grew for the fourth straight quarter in 3Q11, although at the lowest percentage (4%) for those quarters. Of the top ten vendors, ZTE, Cisco, Fujitsu, and Huawei all posted revenue growth compared with 3Q10; NEC was flat; and Tellabs, Alcatel-Lucent, NSN, Ciena, and Ericsson all had revenue declines. For Tellabs, this marked the third year-over-year decline in a row.

Market Share Changes

ZTE gained the most, Alcatel-Lucent lost the most annualized share

Huawei, Alcatel-Lucent, ZTE, Ciena, and Fujitsu remained the top five vendors based on annualized share; all have more than 5% annualized share and more than $1bn in annualized revenues. The share gap between Huawei and Alcatel-Lucent widened in 3Q11 for the first time in over a year as Huawei’s share held steady but Alcatel-Lucent’s slipped. Number three ZTE topped the list of share gainers for the second straight quarter. On the other end, Tellabs continued to struggle as its flagship 5500 bandwidth management business slid further from historic highs: Tellabs, which was the number six ON vendor as recently as late 2010, has dropped a full share point since, has slipped to tenth place, and is in danger of getting knocked out of the top ten by China-based FiberHome. Although NSN and NEC each improved their market ranks, their related share shifts were not significant.