Gartner's Dataquest Insight: Scorecard for Vendors of LTE Network Infrastructure

Release Date:2010-01-12

June 29, 2009 By Sylvain Fabre, Frank Marsala, Jouni Forsman, Tina Tian, Joy Yang, Akiyoshi Ishiwata

An LTE market opportunity has emerged during the past two years. Most vendors now have relatively well-defined solutions, which are scheduled to be ready for initial rollout by the end of 2009. LTE technology may reduce carriers’ operating costs for mobile data — compared with third-generation (3G) technology — as data volumes increase and as mass use of the mobile Internet is enabled by compatible devices and fast, low-latency backhaul.

In this document we evaluate the main vendors of LTE network infrastructure. Some focus on the radio capabilities of their LTE offerings, while others have a more comprehensive view including the evolution of an all-IP core. Other factors that distinguish one vendor from another include the scalability, interoperability and modularity of their products, their ability to deliver and deploy networks, their skills in facilitating carriers’ moves to IP networks, and their perceived viability as companies.

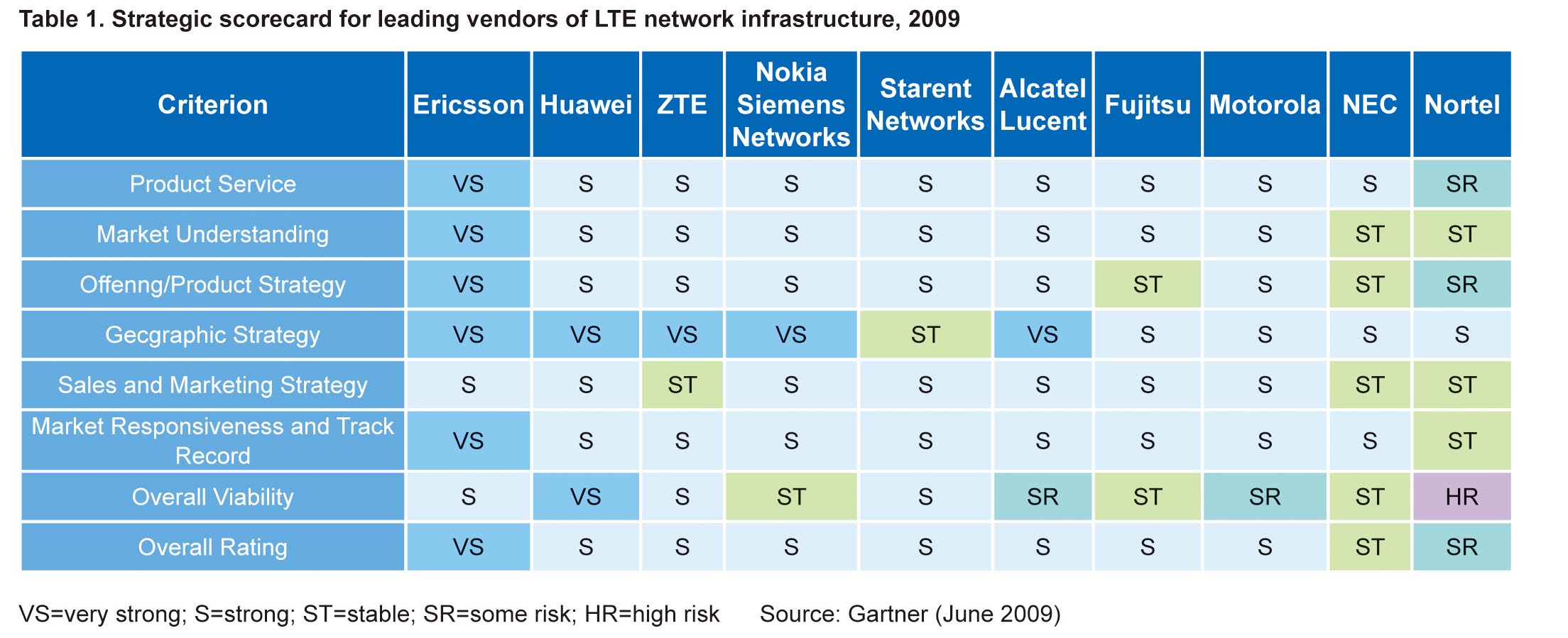

Strategic Scorecard for LTE Network Equipment Vendors, 2009

Gartner rated the qualifying mobile infrastructure vendors using seven standard Gartner criteria on a scale from 1 to 5, with 1 being best and 5 worst. The seven criteria include Product or Service, Market Understanding, Offering/Product Strategy, Geographic Strategy, Sales and Marketing Strategy, Market Responsiveness and Track Record, and Overall Viability. In addition, each criterion was given a numerical weight. The vendors were then ranked according to overall score, with each score rounded up to the nearest digit, and the results color-coded for easier comprehension.

Our comparison of LTE vendors based on these seven criteria yielded the results shown in Table 1. There are several types of vendors in the sample group, and not all are strictly comparable from the perspective of LTE offerings. For example, while Ericsson, Huawei, NSN, ZTE, Alcatel-Lucent and Nortel (at least until the NSN transaction goes through) can be considered end-to-end vendors, others, like Starent (focused on EPC core and without a radio offering) and Motorola (with its own radio product but an EPC from Starent), are more specialized. Hence our ratings aim to capture the overall relative value and attractiveness of each vendor’s LTE offering, regardless of the specific parts of the network being focused on.

Overall Evaluation of Global LTE Network Equipment Market Opportunity

Gartner expects that LTE will become the dominant mobile network technology and that most network operators will upgrade to it. But operators are actively evaluating multiple technology options. Some may choose to extend the life of WCDMA networks by deploying HSPA+, a technology that could support up to 80Mbps download rates in its most sophisticated (and costly) configuration, making it comparable to LTE. This could delay the need for LTE until LTE Advanced (LTE-A) or other fourth-generation (4G) technology options are more widely available (around 2012). Evolution from High-Speed Downlink Packet Access (HSDPA) or High-Speed Uplink Packet Access (HSUPA) to HSPA+ could be less disruptive for operators than moving to LTE, and potentially cheaper too.

But both HSPA+ and LTE will require new client devices as well as upgraded transport infrastructure — consumer and business customers will need to be persuaded to upgrade to high-end handsets and new wireless broadband modems.

Gartner believes that most operators will see the marketing benefits of investing in the latest, fastest technologies, such as LTE, rather than taking the incremental step of upgrading to HSPA+.

Key predictions:

■ LTE will become the dominant 4G technology for CDMA (3GPP2) and GSM/UMTS (3GPP) carriers.

■ More than 70% of UMTS carriers will take every step on the migratory path, including moving to HSPA+ and then LTE.

■ No UMTS carriers will change to WiMAX as their dominant mobile technology.

■ Over 90% of CDMA carriers will adopt LTE.

■ Most cdma2000 deployments will stop at EV-DO Rev. A.

■ More than 90% of WiMAX mobile carriers will not leapfrog to LTE; they will consider upgrades to IEEE 802.16m, if possible.

Overview of ZTE LTE Business

ZTE

ZTE receives an overall rating of Strong for its LTE business.

It has a good set of products. Its growth strategy is prudent and sustainable. ZTE is also getting better at marketing itself outside China, although its strategy for infrastructure remains very regional. This regional focus is partly a positive thing, since Asia/Pacific generally offers good growth opportunities for mobile infrastructure vendors.

ZTE positions itself as an alternative partner for operators for LTE infrastructure. It will mainly focus on North America, Western Europe, Japan and China.

ZTE has been involved in LTE-related work for some years. Before 2006, it was involved in R&D work on MIMO and OFDM technology. In 1Q06, it began participating in research toward the 3GPP standard. In 4Q06, it was among the early group of sponsors joining the Next Generation Mobile Networks (NGMN) Alliance. In 1Q07, ZTE began R&D on LTE, and in 1Q08 demonstrated an LTE prototype live in Barcelona. In 4Q08, ZTE exhibited a pre-commercial LTE system in Beijing. ZTE’s plans for 2010 include a commercial LTE application in the first half of the year.

The company’s product set includes the ZTE Unified Radio Sub-System Platform and OneNetwork platform. ZTE has several form factors planned for eNodeBs: distributed, compact, femtocell and picocell.

ZTE receives a Strong rating for overall viability. This is the result of a strong rating for cash flow (cash from operations as a percentage of revenue for the past 12 months was 8.4%), a good rating for profitability (a net margin of 4.0% in the past 12 months), a strong rating for revenue growth (26.7% in the past 12 months), and a good score for the balance sheet metric that measures solvency (the current ratio is 1.41). The company’s strong financial position has allowed it to maintain its R&D spending at 10% of revenue, which should put it in a good position to capitalize on the growth expected from LTE.

The Impact

■ Although we expect LTE networks to exhibit multivendor scenarios in both core and radio networks, there are too many vendors in this sector at present. We expect further rationalization and fewer vendors as the economic downturn and the trend for reduced capital expenditure continue.

■ Since all but one of the vendors analyzed have a rating of at least Strong for their products, the choice of vendor may hinge more on their perceived overall strength or risk, rather than on technological superiority.

■ Only the leading vendors can sustain the level of R&D necessary for LTE technology to succeed while also enjoying the support of an existing installed base for legacy revenue. This leaves the door open to further mergers and acquisitions.

Ericsson’s LTE business merits an overall rating of Very Strong.

■ The LTE businesses of Huawei, ZTE, NSN, Starent, Alcatel-Lucent, Motorola and Fujitsu each merit an overall rating of Strong.

■ The LTE business of NEC merits an overall rating of Stable.

■ The LTE business of Nortel merits an overall rating of Some Risk.

Conclusion

Ericsson comes out on top in our analysis of LTE network infrastructure vendors. Perhaps the most striking feature of our scorecard is the many vendors, including two from China, with overall ratings of Strong. Most of the vendors analyzed are technically skilled, so the key differentiator may rather be the perceived overall risk profile of a vendor, with the smaller ones, and those whose financial results may be a concern, being viewed by operators as riskier propositions when it comes to choosing a long-term partner for LTE.